Quick and Easy Access to Funds

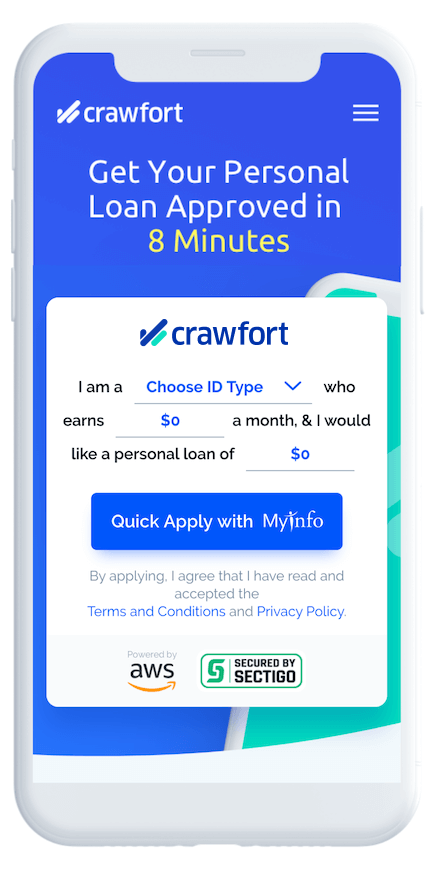

A licensed money lender provides quick and easy application processes, which is ideal for sudden emergencies. It only takes minutes to finish the application, Also, at Crawfort, it only takes 8 minutes to approve your application.

Therefore, disbursing of funds considerably faster; sometimes you may even get the funds that you need on the same day that you have applied.

Flexible Loan Options

A legal private money lender offers a variety of loan products tailored to address different financial needs.

Whether it’s for a short term or long-term needs, lenders offer a wide range of loan options from quick loans, payday loans, loans for medical bills, study loans, wedding loans, travel loans, Grab/Gojek/Taxi loans to any short term loans.

Loans Available to All Income Groups

Looking for a loan but worried about your income? Licensed money lenders often provide loan option even to low-income earners.

They understand that financial needs can arise unexpectedly, that is why they designed loan products to cater to individuals across all income levels.

Building or Rebuilding Credit

For individuals with low credit scores or limited credit history, obtaining a loan from traditional banks can be challenging.

A licensed money lender is often more willing to consider applicants with less-than-perfect credit. By responsibly repaying a loan from a licensed lender, you can demonstrate your creditworthiness and improve your credit score over time.

Providing Transparent and Responsible Lending Practices

Legal lenders value transparency and responsible lending practices. They will clearly explain all loan terms and conditions upfront, including interest rates, fees, and repayment schedules.

Furthermore, they will collaborate with you to ensure that you understand the terms of your loan and can comfortably manage your repayments.

Debt Consolidation

If you’re struggling with multiple debts and high-interest payments, a licensed money lender can help you consolidate them with a debt consolidation loan at a much lower interest rate.

This can simplify your finances, reduce your monthly payments, and make it easier to manage your debt effectively.

Best Licensed Moneylenders in Singapore: Guide to Borrowing Loans from Legal Lenders

Are you short of funds and planning to borrow from the best licensed money lender in Singapore? But before that, you must first understand the

Guide on Borrowing Personal Loan from Toa Payoh Money Lender

Toa Payoh, one of the first HDB (public housing) areas in Singapore, started in the 1960s to sort out housing for a lot of people.

10 Essential Things You Need To Know When Borrowing A Personal Loan From Hougang Money Lender

Singapore’s northeastern residential district, Hougang, borders Punggol to the north, Upper Serangoon Road to the south, Sungei Serangoon to the east, and Yio Chu Kang

Guide To Borrowing From Ang Mo Kio Money Lender: How To Avoid Illegal Lenders

Ang Mo Kio, situated in the northeastern region of Singapore, derives its name from Hokkien, translating to “red-haired man’s bridge.” As a planning area and

Credit Card Or Personal Loan From Licensed Moneylenders: Which Is Better For Financing Your Next Vacation?

When planning a well-deserved getaway, the excitement of exploring new destinations and creating lasting memories can quickly be overshadowed by the financial considerations of funding

How Much Can I Borrow From A Money Lender & What I Need To Note?

The cost of living is high in Singapore. There are times when we inevitably run into money problems and need cash to tide over difficult